As world currencies are tanking against the USD (US Dollar), Bitcoin is holding its ground. A strong USD is creating a debasement as the DXY hit an index high of 114.61. The strength of the USD has increased relative to a basket of other currencies (e.g. British Pound, Japanese Yen, etc.). Since the USD is the global reserve currency, a stronger dollar means higher costs for international trading. This affects prices of commodities that are paid for in USD, because of the exchange rate.

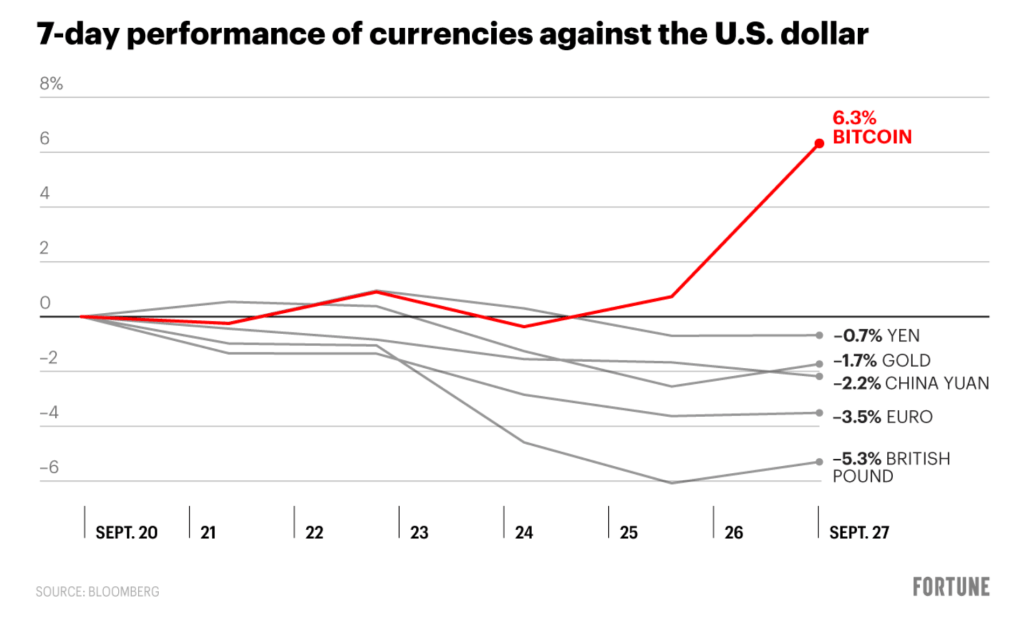

In the last 7 days (as reported on Fortune 9/28/22), Bitcoin has grown 6.3%, hitting $20K+ before eventually settling back to a lower level. Other currencies did not do as well. The biggest losses were the British Pound at -5.3% and the Euro at -3.5%. Even the Yuan was not spared, dropping -2.2%.

Safe haven asset gold did just as poorly as the other world currencies. It has fallen by -1.7% against the USD, while Bitcoin has gone up. At this point it is risk off, and many investors are selling off assets in stocks/equities and moving to the USD. Crypto traders are likewise moving their assets from volatile cryptocurrency to stablecoins (e.g. USDT, USDC) that are pegged to the USD.

To further complicate matters, inflation is getting higher. The US has hiked interest rates in order to combat rising inflation, which kills demand and destroys risk on assets. For many investors crypto is being treated like tech stocks, so there have been many sell-offs regarding that. However, there are still those who believe that Bitcoin can be a way to solve that problem.

The idea behind Bitcoin (per maximalist thinking) is that it could or should be a hedge against inflation or economic uncertainties like currency debasement. That means that Bitcoin should be inversely correlated to inflation, but it has been more correlated to the traditional financial markets. Even though the founder Satoshi Nakamoto never stated that it was Bitcoin’s exact purpose to hedge inflation, it has opened that idea since it is outside the current financial system. It is not state controlled or corporation held, which makes it a neutral store of value. It also has a capped limit (21 million coins), so it cannot increase in supply. Despite this, there are large holders (i.e. whales) who can still manipulate prices.

It is interesting to see how this all plays out. It has been observed over the last few years that a stronger dollar equates to a weaker Bitcoin or BTC. At the moment we are seeing that it is not always the case. People who do not want to lose value in their wealth could start putting their money into crypto like BTC. What is slowly happening is that people from those countries where their currency is getting debased are exploring crypto as a way to preserve their wealth. Perhaps it is a short term trend, but if it remains stable within the next few weeks or months, this could be a sign that the value of BTC is being realized.

Disclaimer: The information provided is for reference and educational purposes only, and is not financial advice. Always DYOR to verify information.